Learn More About the Closing Disclosure

What is the New Closing Disclosure?

The Closing Disclosure is one of the new TRID (TILA-RESPA Integrated) disclosures that will take effect this fall with the implementation of the CFPB’s Know Before You Owe rule. The Closing Disclosure is provided to borrowers within three business days of settlement. A similar form is provided to the seller of the home, less the details of the borrower’s mortgage loan.

The Closing Disclosure will combine two forms that are in use now – the late Truth-in-Lending form and the HUD-1. Confusion will be reduced by combining and simplifying the required disclosure information into one form.

What is Purpose of Closing Disclosure?

The Closing Disclosure has four basic purposes:

- To describe the costs you’ll pay at closing over the life of your loan

- To compare these costs and your pre-paid expenses to those listed in your written Loan Estimate

- To highlight certain loan terms (such as how a late payment is handled)

- To provide contact information for the primary professionals involved in your real estate transaction

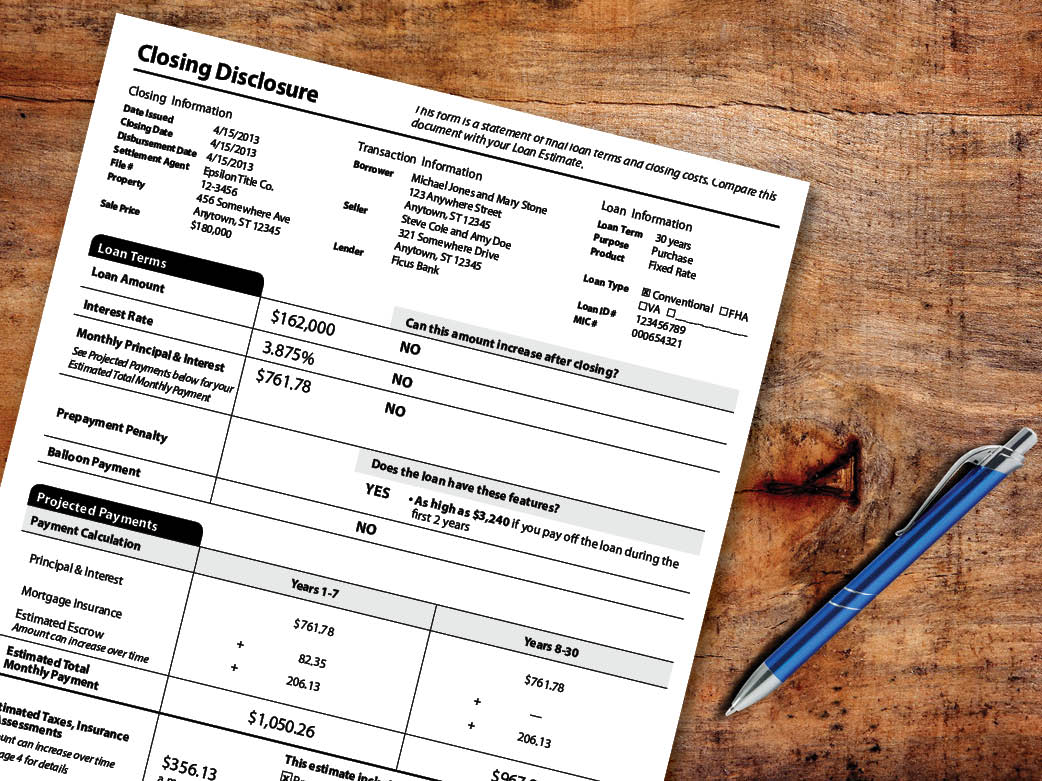

Here is a sample Closing Disclosure as provided by the Consumer Finance Protection Bureau: Sample Closing Disclosure

Revised Closing Disclosures

As stated, borrowers will receive the Closing Disclosure within three business days of settlement. If certain loan changes occur, you will receive a revised Closing Disclosure. Receipt of revised Closing Disclosure must occur three business days prior to settlement. More specifically, a change in loan program, a change in APR beyond specific tolerance levels, or an addition of a pre-payment penalty will require re-disclosure and potentially delay a closing.

New Closing Disclosure Effective Date

The CFPB recently proposed that the implementation of the new disclosures and regulations be delayed for two months. Instead of August 1, 2015, the CFPB has proposed that the effective date for TRID be moved to October 3, 2015 – see the CFPB news release here. While that date may seem far away, Realtors, lenders and Settlement Service providers must adjust their systems and processes to adhere with new rules.

Please check back here often for more information on TRID disclosures, rules, pending changes and implementation dates. As always, our goal is to provide our borrowers and business partners with exceptional lending services – preparing our partners and borrowers for TRID will help ensure a smooth transition for all involved.

Please do not hesitate to ask a question – email info@inlanta.com for more information or find a loan officer near you using our branch locator.

About Inlanta Mortgage

Headquartered in Brookfield, Wisconsin, Inlanta Mortgage is a growing mortgage banking firm committed to quality mortgage lending, ethical operations and strong customer service.

Inlanta Mortgage offers Fannie Mae/Freddie Mac agency products, as well as a full suite of jumbo and portfolio programs. The company is an agency approved lender for Freddie Mac and Fannie Mae, FHA/VA, FHA 203K and USDA. Inlanta Mortgage also offers numerous state bond agency programs. Review Inlanta’s mortgage loan programs.

Inlanta Mortgage was recently named a Top Workplace for a third time in 2015. Inlanta has also received the Platinum Million Dollar USDA Lender Award and has been recognized as a Top Mortgage Employer by National Mortgage Professional and a Top 100 Mortgage Banking Company and 100 Best Mortgage Companies to Work For by Mortgage Executive Magazine.

Inlanta Mortgage, Inc. NMLS #1016